Web3 without seed phrase: smart wallets and traceable money

How Web3 leaves the seed phrase behind and enters the era of smart wallets, passkeys and verified identity on the way back to the bank.

For years, Web3 sold a simple promise: "be your own bank".

The phrase sounded powerful. Independence. Sovereignty. Direct control over money.

But the technical reality was much less comfortable.

Being your own bank meant safeguarding a 12 or 24-word phrase, understanding what you were signing, telling a legitimate wallet from a fake one, paying gas in the right token, surviving bridges, exchanges, contracts, infinite permissions and phishing links. For a technical minority, that was freedom. For the average user, it was a trap dressed as innovation.

In 2026, Web3 has not disappeared. Nor has it magically become safe. What is happening is more interesting: the ecosystem is changing its architecture. Security no longer depends only on a person not losing a secret phrase, and is moving toward programmable accounts, passkeys, smart wallets, recovery rules, regulated providers and tax traceability.

The thesis of this article is simple:

Web3 has not eliminated trust. It has changed where it is placed, who verifies it and what documents it requires when money returns to the banking system.

That change has two sides.

The first is technical: Ethereum and its ecosystem are trying to make wallets less primitive. The second is regulatory: Europe and other jurisdictions are closing the era of opacity in the entry and exit between crypto-assets and fiat money.

The seed phrase is no longer the absolute center of the story. The new center is something else: proof.

Proof of account control. Proof of authorization. Proof of source of funds. Proof of identity. Proof for tax purposes. Proof that the money has a defensible history.

1. The original problem: an Ethereum account was not an account, it was a key

Imagine your bank account was, literally, a physical key. The key opens the box. If you lose it, there is no bank to call. If someone steals it, the thief becomes the owner. No daily limit, no alert, no way back. That is, in essence, what an Ethereum account has been for years.

On Ethereum, for years, the basic account has been the EOA: Externally Owned Account. That is, an account controlled by a private key. If you have the key, you control the account. If you lose the key, you lose access. If someone steals the key, they control the funds.

That model has one advantage: it is simple.

But it has a serious flaw: it is brutal.

There is no native recovery. There are no default spending limits. There is no real second factor built into the account. There is no flexible permission logic. There is no human way to tell, from the account itself, between a routine operation and a dangerous one.

The traditional account works like an absolute lock. Open or closed. Alive or dead. Full control or full loss.

That is why account abstraction was born: the idea that an account should not be just a key, but a programmable piece able to define its own rules. The ERC-4337 standard introduces this model without modifying Ethereum's base protocol: it uses objects called UserOperation, an alternative mempool, and an EntryPoint contract that coordinates validation and execution.

In simple terms: instead of the user signing a classic transaction directly from an EOA, the user's intention becomes an operation that can pass through more logic before being executed.

That makes it possible to build wallets with features a traditional account does not handle well: social recovery, spending limits, sponsored gas payments, batched operations, validation with other authentication methods, and more granular security policies.

The wallet stops being a key.

It starts to look like a programmable safe.

2. ERC-4337: the account starts behaving like software

ERC-4337 does not eliminate every risk. But it does change the architecture.

In this model several new pieces appear:

- UserOperation: not a normal transaction. It is a user's intention with additional information for validation, execution and payment.

- Bundler: collects user operations and sends them to the network.

- EntryPoint: the contract that processes those operations, validates whether they are acceptable, and coordinates their execution.

- Paymaster: can allow someone other than the user to pay the gas, or let gas be covered in more flexible ways.

Translated to everyday life: it is the difference between handing someone your card and PIN, or giving them permission to spend €50 per day at a specific store. The traditional account only knew the first option. The new ones know the second as well.

The ERC-4337 documentation describes exactly this flow: an account abstraction system based on UserOperation, an alternative mempool, and EntryPoint, without needing to change Ethereum's base protocol.

The improvement in user experience is clear: users can interact with applications without having to understand every detail of gas, without holding ETH exclusively for fees in every case, and with wallets that can include their own rules.

But it must be said precisely: this does not automatically make Web3 safe.

It only shifts the risk surface.

Before, the main risk was losing or exposing a private key. Now, on top of that, you have to watch the contract logic, the bundler's behavior, the paymaster's configuration, the modules installed in the account, and the interface that shows the user what is being signed.

It is not less security.

It is more complex security.

3. EIP-7702: Ethereum tries to rescue legacy accounts

The big practical problem of smart accounts is that millions of users already had EOA accounts, funds, history, identities, ENS, permissions and activity. Asking them to migrate everything to a new wallet was a huge barrier.

That is where EIP-7702 comes in.

Ethereum.org describes EIP-7702 as a mechanism to add code to an EOA through a new transaction type, type 4, which includes an authorization list. In practical terms, it allows a traditional externally owned account to delegate behavior to code that is already deployed.

The Pectra upgrade was activated on Ethereum mainnet on May 7, 2025, and Ethereum.org presents it as an important step toward broader account abstraction.

This part matters, because a common exaggeration should be avoided here: EIP-7702 does not mean an EOA stops depending on its original private key. The EOA can delegate behavior, but the authorization remains critical. If the user authorizes wrongly, if the interface deceives them, if the delegated code is dangerous, or if the wallet does not protect that flow well, the risk does not go away.

The promise is strong: giving smart account capabilities to existing accounts without forcing users to move all their funds.

So is the danger: a bad delegation can turn a usability improvement into an attack vector.

That is why the message should not be "EIP-7702 makes wallets safe". The correct message is different:

EIP-7702 modernizes EOAs, but it forces wallets to explain and protect, much better, what code is being authorized.

4. The death of the seed phrase is not total, but it has begun

For years, the seed phrase was treated as a rite of passage. If you could not safekeep 12 or 24 words, Web3 was not for you.

That approach was a product disaster.

A technology that requires the average user to safeguard a secret phrase as if they were a system administrator is not mature technology. It is a transfer of responsibility: the protocol protects itself, but leaves the user alone in front of human error.

Smart accounts and passkeys try to correct that legacy.

WebAuthn, a W3C specification, defines a standard way to create and use cryptographic keys on the user's device, tied to a specific site or service (the Relying Party, which in plain language is the website or app that trusts that key to recognize you). The credential is created and stored in an authenticator (the phone, a hardware key, or the operating system itself), with the user's consent, and can only be used by the origin that created it.

This allows the use of passkeys, local biometric unlock, or hardware authenticators without turning the user's fingerprint or face into data published on a blockchain.

And here it must be made very clear:

There is no such thing as "on-chain biometrics" in the loose sense of the expression. The fingerprint or face does not go to the blockchain. What happens is that the device uses a local gesture (for example Face ID or fingerprint) to unlock a key or credential, and a cryptographic proof is then produced.

This difference is essential. If it is communicated badly, it turns into smoke. If it is explained well, the real improvement becomes clear: the user can authenticate more conveniently without exposing their biometrics to the contract.

Even so, the absolute end of seed phrases should not be oversold. They still exist. They are still in use. Many wallets keep them. Many architectures still depend on keys that can be recovered through seed phrases.

What can be said with rigor is this:

The seed phrase is no longer the only conceivable interface for self-custody. In 2026, smart accounts, passkeys and programmable recovery systems offer a real alternative, though not yet a universal one.

5. Invisible security does not mean nonexistent security

There is a dangerous idea in technology: believing that if something becomes easy, it also becomes safe.

Not always.

For readers who want to bring this risk layer down to concrete threats (phishing, permissions, wallet drainers, and operational mistakes), there is a specific guide on protecting cryptocurrencies against real threats. Along the same line of pre-signing defense, a free utility such as Brújula Security, an extension for Chromium browsers, warns when a crypto site is not verified or imitates another one through typosquatting. The focus here is different: how the architecture of the account changes.

Smart wallets improve the experience, but they also introduce new layers that have to be audited. A programmable wallet can have spending limits, social recovery and advanced rules. But it can also have bugs, insecure modules, permissions that are too broad, or external dependencies.

The old Web3 had a visible problem: do not lose your words.

The new Web3 has less visible problems: trust that this module, this contract, this bundler, this recovery policy and this interface are well designed.

That does not mean the new architecture is worse. It means the type of diligence changes.

Before, the user had to protect a key.

Now the ecosystem has to protect a system.

And when a system becomes more complex, audit stops being optional.

This is where the technical narrative gains strength: account abstraction is not just a UX improvement. It is a redistribution of risk. It removes friction from the user, but forces wallets, infrastructures and developers to take on more technical responsibility.

In other words: Web3 looks less like keeping gold under the mattress and more like operating a programmable financial infrastructure.

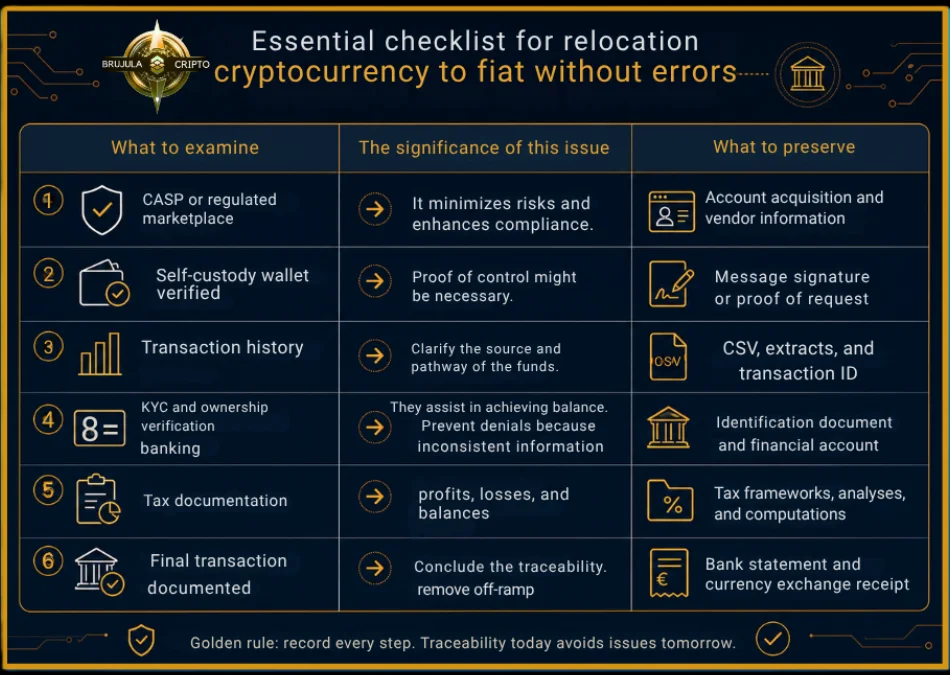

6. The other side of the system: going out to fiat

Most debates about Web3 focus on getting in: buying crypto, creating a wallet, signing a transaction, using DeFi.

But the most important moment is usually a different one: getting out.

Turning digital assets into euros, dollars or bank money is not a simple click. It is the point where crypto money touches the traditional financial system. And there, the rules change.

When the money returns to the bank, owning it is not enough anymore. You have to be able to explain where it came from, where it went through, which platform was involved, which identity operated it and what tax obligations it might generate.

This is where the other great transformation of 2026 comes in: regulatory institutionalization.

In the European Union, MiCA is no longer a future promise. ESMA explains that the MiCA rules cover the issuance, public offering, admission to trading and provision of services on crypto-assets in the EU.

In addition, ESMA published in April 2026 a specific statement on the end of MiCA's transitional periods. The key point: the transitional period expires across the European Union on July 1, 2026. By that date, unauthorized CASPs (crypto-asset service providers: exchanges, custodians, regulated platforms) must have implemented their orderly wind-down plan.

This changes the tone of the market.

Before there were more grey zones. Now there is a clearer regulatory border.

A provider can be authorized or not. A user can have more or less protection depending on who they operate with. An off-ramp can come from a supervised entity or from an origin that is much harder to defend.

7. MiCA does not make the entire ecosystem safe, but it shifts the burden of proof

It is wise not to overstate MiCA.

In order not to repeat here a full guide to regulation, this section pairs with the previous analysis on the new global crypto regulation. Here the focus is more concrete: what changes when the money wants to return to the bank.

MiCA does not turn every token into a safe one. It does not eliminate market risk. It does not prevent every fraud. It does not guarantee that a user will not lose money. It does not turn a bad investment into a legitimate asset.

What it does do is establish a framework for issuers, providers and services on crypto-assets within the European Union. That has direct consequences for exiting to fiat.

When a user tries to move money from an exchange to a bank, the bank no longer just sees a transfer. It sees a compliance history.

Is the provider authorized? Does the identity match? Does the transfer come from an account in the same holder's name? Is the operation documented? Can the user justify acquisition, sales, gains, losses or economic activity? Are there signs of structuring or opaque routes?

It is not necessary to claim that every banking entity cross-checks every transfer in real time against a technical ESMA registry. That claim would be too specific without public official proof.

The correct version is more sober and more defensible:

Since the end of MiCA's transitional period, the European user has a clearer way to distinguish between authorized and unauthorized providers. That distinction does not eliminate the bank's analysis, but it does change the compliance context of the off-ramp.

This nuance matters. It prevents a serious investigation from turning into a claim that is impossible to prove.

8. Travel Rule: self-custody enters the verification zone

Another key change is the Travel Rule applied to crypto-assets.

The European Banking Authority published guidelines on information requirements in transfers of funds and certain crypto-assets under Regulation (EU) 2023/1113. These guidelines specify the steps for payment providers, CASPs and intermediaries to detect missing or incomplete information in transfers of funds or crypto-assets.

Austria's FMA, the country's financial supervisor, sums up an important practical point: in transfers from or to a self-custodied wallet for an amount above 1,000 euros, the CASP or the ICASP (intermediary that executes the transfer between providers) must check whether that address belongs to the client or is controlled by them.

This does not mean self-custody is forbidden.

It means self-custody stops being invisible when it touches a regulated provider.

That point is decisive.

For years, part of the crypto narrative assumed that owning a wallet was a kind of sovereign zone outside the system. Technically, you can control an address. From a regulatory standpoint, if you want to enter or exit through an obliged provider, that address may have to be linked to your identity.

The message for the user is clear:

Controlling a wallet is not enough. In relevant operations, you may also need to prove that the wallet is yours.

This completely changes the documentary hygiene of the crypto user. Loose screenshots, scattered movements, or vague explanations about having had it for years are no longer enough. The user needs traceability.

9. The mistake of microtransfers: splitting does not cleanse

One of the most dangerous myths of the off-ramp is thinking that a large operation becomes less suspicious if it is split into many small ones.

This should not be presented as operational advice to avoid controls. On the contrary: it must be explained as a risk signal.

The logic of financial compliance does not look only at isolated amounts. It looks at patterns, frequency, origin, destination, identity, relationships between accounts, and economic coherence.

Therefore, the editorial message must be responsible:

There is no official basis for claiming that breaking funds into pieces avoids bank controls. In financial compliance, structuring can be read as a risk signal, not as a solution.

This point protects the article from becoming a dangerous guide. It also reinforces the editorial line: no shortcuts are published; autopsies are.

10. DAC8 and CARF: the year the data starts being organized

Regulation is not limited to the provider's license. Taxation comes in too.

DAC8 introduces automatic exchange of information on crypto-assets within the European Union. The European Commission explains that reporting providers send the information to their national tax authorities in the year following the reported period, and that the exchanges concerning the first year of reporting will take place before September 30, 2027.

Translated: 2026 is the year that gets collected; 2027 is the year when that information starts circulating between administrations.

This is a profound change.

For a long time, the crypto user could act as if their activity depended on their own voluntary declaration. That scenario is narrowing. Obligated platforms collect data, the authorities receive information, and the capacity for cross-checking grows.

The practical consequence is not that every user is suspicious.

The practical consequence is that documentary improvisation becomes much more dangerous.

A user who buys, sells, swaps, withdraws, deposits and crosses platforms needs to reconstruct the history. And the more time has passed, the harder it will be to do it if no records were kept.

In 2026, for anyone operating with regulated ramps, traceability stops being an accounting recommendation and becomes a practical condition for avoiding rejections, reviews or blocks.

11. Spain: 721, 172 and 173 as a tax infrastructure for traceability

In Spain, the Tax Agency already has specific information forms related to virtual currencies.

Form 721 refers to virtual currencies located abroad. The Tax Agency itself maintains the procedure for form 721, "Informative declaration on virtual currencies located abroad".

In addition, the Tax Agency hosts on its electronic office forms 172 and 173: form 172 as an informative declaration on balances in virtual currencies, and form 173 as an informative declaration on operations with virtual currencies.

This does not authorize one to say that the bank automatically queries all those forms before accepting a transfer. That sentence would be too specific without official banking proof.

What can be said is more solid:

Spain already has a specific tax infrastructure to declare balances and operations with virtual currencies. That infrastructure increases the traceability available and shrinks the room for treating cryptocurrencies as an informal tax territory.

The difference between the two sentences is enormous.

One invents a universal banking process.

The other describes an official fact.

12. Proof of Reserves is not Proof of Funds

Another common confusion is mixing three concepts:

- Proof of Reserves: evidence that an exchange holds sufficient or verifiable reserves against certain balances.

- Proof of Funds: documentation that proves a specific person has funds available.

- Source of Funds / Source of Wealth: explanation and evidence of the economic origin of those funds.

They are not the same.

An exchange can publish proof of reserves, even with cryptographic structures like Merkle trees, and that can improve the custodian's transparency. But that does not automatically prove that a specific user's money has an origin that is fiscally defensible before a bank.

Proof of reserves speaks about the exchange.

Proof of funds speaks about the user.

Proof of source of funds speaks about the economic history.

This nuance has to appear because it prevents one of the sector's most common exaggerations.

The banking question is usually not only whether those funds exist.

The real question is where they come from, how they were obtained, what documentation supports them, and whether they fit the client's profile.

That is the new friction point.

13. The paradox: Web3 wanted to eliminate intermediaries, but now it needs better proof

Here the central paradox appears.

Web3 was born with an anti-intermediary impulse: do not trust banks, do not depend on platforms, do not ask for permission. But the real experience of 2026 shows a more ambiguous architecture.

In pure self-custody, the user can still control keys.

But on the entry and exit to fiat, the user runs into CASPs, banks, regulators, tax forms, Travel Rule, self-custodied wallet checks, and origin documentation.

The intermediary does not disappear.

Its role changes.

Before, the intermediary held custody and decided.

Now the intermediary verifies, reports, classifies, and can block or request additional information when it does not understand the story.

Technical sovereignty does not eliminate financial traceability.

This is the point that must be remembered:

You can control a wallet and still not be able to move that money comfortably into the banking system if you cannot explain its history.

That sentence sums up the cultural shift.

14. Security is no longer about hiding, but about documenting

For years, many crypto users thought of privacy as the absence of records.

In the regulated off-ramp, the opposite happens: the lack of records can become the problem.

A good exit to fiat does not depend only on choosing a known exchange. It depends on having a documented sequence:

- when it was bought;

- from which account;

- on which platform;

- with which identity;

- what operations were carried out;

- what fees there were;

- what sales were made;

- what gains or losses were generated;

- what tax filings apply;

- what final transfer arrives at the bank.

The new maturity of Web3 is not measured only by how easy it is to open a wallet.

It is measured by the capacity to close the loop without the money becoming inexplicable.

In a system like this, documentation stops being secondary bureaucracy. It becomes part of security.

15. Conclusion: Web3 did not die; it became auditable

The easy narrative would be to say that Web3 failed.

That is not accurate.

Web3 has not died. But it has lost part of its narrative innocence. The idea that a wallet, a seed phrase and a promise of decentralization were enough has fallen short.

In 2026, the ecosystem moves in two directions at once.

On one side, the technical infrastructure tries to correct the usability mistakes: programmable accounts, passkeys, EIP-7702, ERC-4337, social recovery and wallets that are less dependent on seed phrases.

On the other, the regulatory infrastructure demands more traceability: MiCA, Travel Rule, DAC8, tax forms, provider verification and proof of control over self-custodied wallets.

The consequence is uncomfortable but clear:

Web3 can no longer sell freedom alone. It has to demonstrate security, traceability and operational responsibility.

The seed phrase represented a primitive stage: the user alone before their key.

The programmable account represents a second stage: the user protected by rules.

The regulated off-ramp represents a third: the user required to prove the history of their money.

That is the real change.

We are not facing the end of Web3.

We are facing the end of Web3 without papers.

And perhaps that is the most important autopsy: decentralization does not eliminate proof. It only delays the moment someone demands it.

ApisDom, for Brújula Crypto. Editorial analysis on the technical and regulatory transition of Web3 in 2026.

Editorial summary

In 2026, Web3 changes phase. The seed phrase stops being the absolute center, Ethereum advances with ERC-4337 and EIP-7702, and the exit to fiat is increasingly conditioned by MiCA, Travel Rule, DAC8 and tax traceability.

Verified official and technical sources

| Source | Link |

|---|---|

| ERC-4337 (Account Abstraction Using Alt Mempool) | eips.ethereum.org |

| Ethereum.org: Pectra 7702 guidelines | ethereum.org |

| Ethereum.org: Prague-Electra (Pectra) | ethereum.org |

| W3C: Web Authentication Level 3 | w3.org |

| ESMA: Markets in Crypto-Assets Regulation (MiCA) | esma.europa.eu |

| ESMA: Statement on the end of transitional periods under MiCA (April 17, 2026) | esma.europa.eu (PDF) |

| EBA: Guidelines on information requirements (Regulation EU 2023/1113) | eba.europa.eu |

| FMA Austria: Transfer of Funds Regulation (TFR) | fma.gv.at |

| European Commission: DAC8 | taxation-customs.ec.europa.eu |

| AEAT: Form 721 (virtual currencies abroad) | sede.agenciatributaria.gob.es |

| AEAT: Form 172 (balances in virtual currencies) | sede.agenciatributaria.gob.es |

| AEAT: Form 173 (operations with virtual currencies) | sede.agenciatributaria.gob.es |

Related articles

%2FPORTADA%20brujulacrypto.png?alt=media&token=8f4ce7fc-a784-4913-9007-0aa92f78aa62)

Goodbye to the Crypto "Wild West": The Ultimate MiCA Survival Guide (2025)

MiCA is the European crypto regulation in force since December 2024. It mandates reinforced KYC on exchanges, private wallet verification (over €1,000), Travel Rule with zero threshold and White Paper approval for stablecoins. Affects Kraken, Coinbase, Binance and Bitpanda users with new proof-of-funds requirements.

Ultimate 2026 Guide: How to Shield Your Crypto from Phishing, Wallet Drainers and Deepfake Scams

Prioritize protecting your seed phrase. Keep most of your funds in a cold wallet and adopt a mindset of total distrust toward promises of easy money. Being your own bank isn't an option, it's an inescapable responsibility if you don't want to become a statistic.

Protect Your Crypto: 5 Real Threats You Must Avoid

Billions stolen in crypto scams. Most via social engineering. Discover the 5 real threats and proven strategies to protect your Bitcoin and crypto

Tags

Comments

What did you think about this article?

Share your experience and help fellow crypto navigators.

Information That Protects Your Capital.

Stay protected: receive free monthly alerts about new crypto threats, exclusive security guides, and practical resources to safeguard your funds. Your shield against fraud.